How ASC 606, Section 174A, and the 'Kill Switch' Built the AI Ouroboros

By Ryan Wentzel

7 Min. Read#finance#AI#regulatory-arbitrage#accounting#corporate-finance

Table of Contents

- Introduction: The Financial Engineering Boom

- I. The Revenue Engine: ASC 606 and the "Round Trip"

- II. The Antitrust Invisibility Cloak: The "Reverse Acqui-hire"

- III. The Tax Accelerant: OBBBA and Section 174A

- IV. The Shadow Leverage: The "Kill Switch" and GPU Surveillance

- V. Conclusion: The "Cisco" Moment?

Introduction: The Financial Engineering Boom

The dominant narrative of 2025 is that we are living through an Artificial Intelligence boom. A forensic review of the capital flows suggests we are actually living through a Financial Engineering boom.

While the public fixates on context windows and agentic benchmarks, the real innovation is happening in the legal departments of Redmond, Mountain View, and Roseland, NJ. Through a masterful combination of "round-trip" revenue recognition, antitrust evasion via "reverse acqui-hires," and the "Subprime for Silicon" debt structures, Big Tech has constructed a circular economy.

This isn't fraud. It's something much more impressive: Regulatory Arbitrage at sovereign scale.

Here is the technical anatomy of the AI Ouroboros.

I. The Revenue Engine: ASC 606 and the "Round Trip"

The heart of the AI economy is the recycling of capital from the balance sheet of a HYPERSCALER (Microsoft, Amazon, Google) to the income statement of that same HYPERSCALER, laundered through a STARTUP (OpenAI, Anthropic, CoreWeave).

The Mechanism

The flow is elegantly simple:

- Injection: Hyperscaler invests $10B into Startup (often in "credits" or cash with restricted use)

- Conversion: Startup uses capital to buy Compute from Hyperscaler

- Recognition: Hyperscaler books $10B as "Cloud Revenue"

Why It's Not Fraud (Technically)

Under ASC 606 (Revenue from Contracts with Customers), this practice is legal provided the contract has "commercial substance." The argument is that the cloud services (Azure/AWS) are distinct goods with standalone value.

However, the magic lies in Equity Method Accounting (ASC 323).

The Arbitrage: When Microsoft owns ~49% of OpenAI, it picks up 49% of OpenAI's losses. But these losses are recorded "Below the Line" (in Other Income/Expense).

The Benefit: The revenue Microsoft receives from OpenAI (Azure spend) is recorded "Above the Line" (Operating Income).

Result: Microsoft subsidizes its own revenue growth. The cost of the subsidy is buried in non-operating expenses, while the "growth" boosts the metrics that drive stock compensation and P/E multiples.

Impact Analysis

| Metric | Impact of "Round Trip" Deal | Investor Perception |

|---|---|---|

| Cloud Revenue | ⬆ Increases | "Hypergrowth" |

| Operating Income | ⬆ Increases | "High Margins" |

| Net Income | ⬄ Neutral (Revenue - Equity Loss) | "One-time investment costs" |

II. The Antitrust Invisibility Cloak: The "Reverse Acqui-hire"

In 2024, the FTC signaled it would block major tech acquisitions. In response, Big Tech invented the "Reverse Acqui-hire."

The Loophole: 16 C.F.R. § 801.2

The Hart-Scott-Rodino (HSR) Act requires reporting of asset acquisitions over a certain threshold. However, a non-exclusive license is not considered an asset transfer because the seller retains the right to use the IP.

The Playbook

The strategy unfolds in four steps:

- Don't buy the company. That triggers HSR and Section 7 Clayton Act review.

- Hire the Founders & Staff. Offer massive compensation packages to the CEO and top researchers.

- License the IP. Pay the "shell" company a massive fee for a "non-exclusive" license to their weights.

- Redeem Investors. The shell company uses the license fee to pay back VCs.

The Reality

The startup is gutted. The "non-exclusive" license is a fiction because the startup no longer has the staff to compete. But on paper, it's just a vendor agreement and a hiring spree.

This structure has been deployed multiple times in 2024-2025, allowing hyperscalers to effectively acquire AI companies without triggering regulatory review. The letter of the law is satisfied while its spirit is systematically circumvented.

III. The Tax Accelerant: OBBBA and Section 174A

The "One Big Beautiful Bill Act" (OBBBA), signed July 4, 2025, fundamentally altered the unit economics of the AI bubble by reversing the punitive R&D amortization rules of the 2017 TCJA.

The "License Fee" Write-Off (Section 174A)

The new law restores immediate expensing for domestic R&D. Google can deduct the entire $2.7B Character.ai license fee immediately. At a 21% corporate rate, this is a $567M tax subsidy from the US Treasury to fund the consolidation of AI talent.

The Hardware Bailout (Section 168(k))

100% Bonus Depreciation is retroactively restored. CoreWeave and Hyperscalers can write off 100% of their Nvidia H100/Blackwell purchases in Year 1, creating massive Net Operating Losses (NOLs) that shield the "round-trip" revenue from taxation.

The combined effect is profound: the federal government is effectively co-investing in the AI buildout through foregone tax revenue, while the accounting treatment makes these investments appear as operating expenses rather than capital allocation decisions.

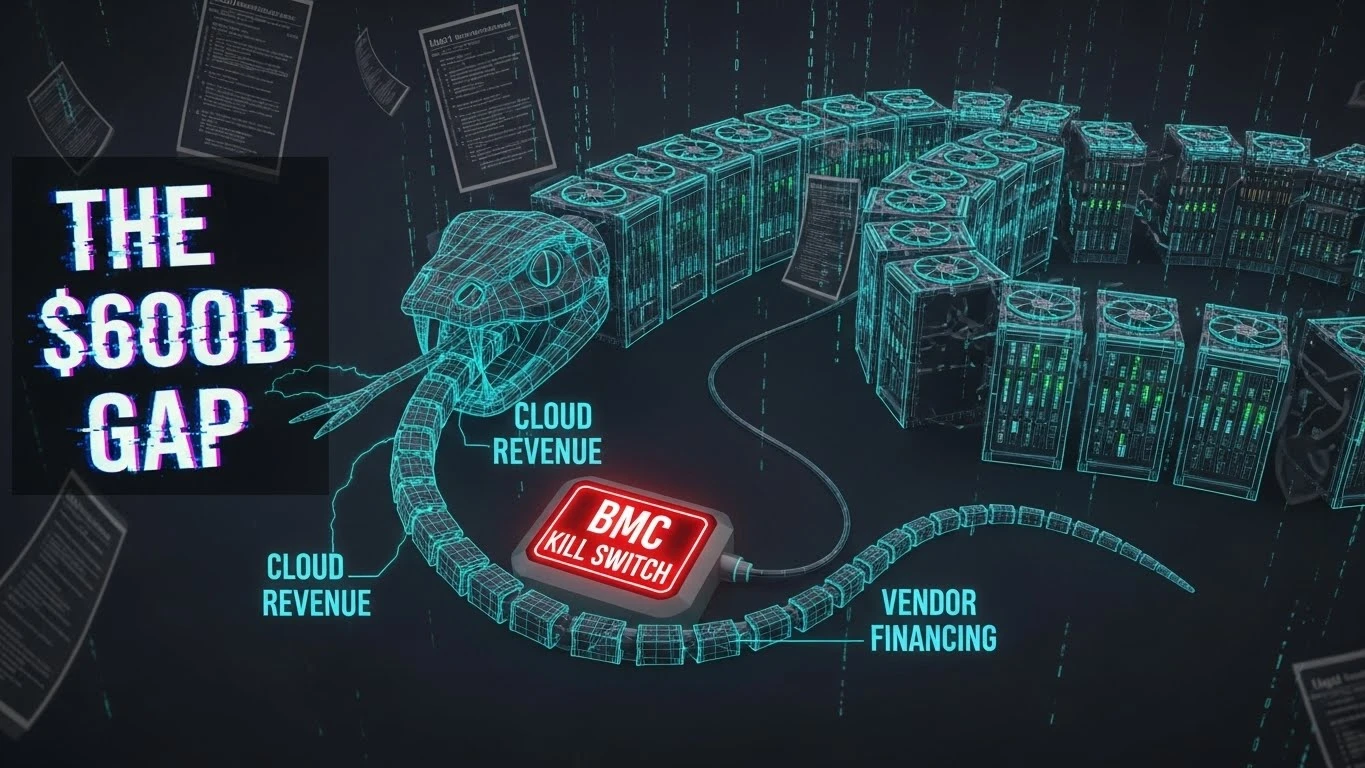

IV. The Shadow Leverage: The "Kill Switch" and GPU Surveillance

With equity markets getting skeptical, the build-out is now funded by Asset-Backed Securitization (ABS) of GPUs. The CoreWeave / Blackstone debt deal introduces a mechanism unprecedented in corporate finance: The Kill Switch.

This isn't just a legal clause; it is a literal, technical backdoor that treats massive AI supercomputers like subprime car loans with remote shut-off devices.

4.1 The "Kill Switch": How it Technically Works

In a typical corporate default, lenders fight in court to seize assets. In this deal, lenders (Blackstone, Magnetar) negotiated the ability to seize control immediately.

TECHNICAL NOTE: The BMC Credentials

The lenders hold escrowed credentials for the Baseboard Management Controller (BMC) of the servers. The BMC is a specialized service processor inside the server that functions even if the main operating system is down. It controls power, cooling, and hardware settings at the bare metal level.

The Trigger: If CoreWeave breaches a covenant (e.g., misses a payment or fails a liquidity test), the lenders can use these credentials to remotely command the H100 GPUs to power down or "brick" (render unusable).

Why brick them? To prevent "asset stripping." If CoreWeave were going bankrupt, they might try to secretly move the GPUs to another location or run them into the ground with 100% load to squeeze out last-minute revenue. The kill switch freezes the assets instantly so they can be repossessed in prime condition.

4.2 "Daily Telemetry": Surveillance Capitalism for Chips

CoreWeave does not just owe money; it owes data. The loan covenants require Daily Telemetry reporting. This is effectively a "heartbeat" monitor for the collateral.

Identity: Cryptographic signatures (device certificates) confirm the specific H100 chips promised as collateral are physically present in the rack.

Health: Temperature, error rates, and clock speeds are monitored to ensure the asset isn't being degraded.

The "Liquidation Playbook": If a default occurs, lenders don't just sell a "box of used chips." They use this telemetry history to grade the chips (e.g., "Grade A" chips that ran cool and stable vs. "Grade B" chips that were overclocked). This maximizes the resale value in an auction.

4.3 The "Loop": The Financial Circularity

The "kill switch" exists because the financial structure is highly circular and risky. This is the CoreWeave / Blackstone / Nvidia Loop:

- Nvidia invests in CoreWeave (giving them equity capital and "allocation" priority for scarce chips)

- CoreWeave borrows billions from Blackstone/Magnetar using that status

- CoreWeave buys Nvidia H100 GPUs with the borrowed money

- Nvidia books revenue, boosting its stock price

- The Collateral for the loan is the Nvidia GPUs themselves

The Systemic Risk: The loan is secured by the very asset that is being mass-produced by the company backing the borrower. If Nvidia releases a new chip (like Blackwell) that makes the H100 obsolete, the value of the collateral crashes. If the collateral value crashes, CoreWeave breaches its "Loan-to-Value" covenants. If covenants are breached, the kill switch is triggered.

Comparison: Traditional vs. Kill Switch Lending

| Component | Traditional Corporate Loan | CoreWeave "Kill Switch" Loan |

|---|---|---|

| Collateral | Factory, Land, IP | H100 GPUs (Depreciating Asset) |

| Default Process | Months/Years of Litigation | Instant Remote Shutdown |

| Monitoring | Quarterly Financial Reports | Daily Hardware Telemetry |

| Control | Legal Liens | Escrowed Root Access (BMC) |

V. Conclusion: The "Cisco" Moment?

We are witnessing a "synthetic" economic event.

- Revenue is synthesized via Equity Method arbitrage

- M&A is synthesized via Licensing Agreements

- Profit is synthesized via Tax Credits (OBBBA)

The system works perfectly until the credit markets stop accepting silicon as collateral. When the depreciation curve of an H100 intersects with the debt service of a CoreWeave SPV, the Ouroboros will choke.

The parallels to the 2000 Cisco moment are striking. At its peak, Cisco was valued at $555 billion—the most valuable company in the world—based on the assumption that internet infrastructure buildout would continue indefinitely. The equipment itself was the collateral for a massive credit expansion. When demand normalized and inventory piled up, the collapse was swift and brutal: an 86% decline in market cap.

The AI Ouroboros faces a similar structural vulnerability. The difference is that the financial engineering is now far more sophisticated, the leverage is embedded in structures that don't appear on corporate balance sheets, and the regulatory arbitrage has created an illusion of organic growth.

When the serpent finally swallows its own tail, the unwind will be equally elegant—and equally devastating.

About Ryan Wentzel

Ryan previously served as a PCI Professional Forensic Investigator (PFI) of record for 3 of the top 10 largest data breaches in history. With over two decades of experience in cybersecurity, digital forensics, and executive leadership, he has served Fortune 500 companies and government agencies worldwide.

Related Articles

Taming the LLM: Using Finite-State Machines to Prevent Hallucinations in AI Workflows

Hallucinations are not a prompt problem—they are an architecture problem. Here is how wrapping LLM calls in a Finite-State Machine transforms a probabilistic model into a predictable, inspectable software component you can ship to paying customers.

6 Min. ReadRead more →

Embracing the Cycle: A Pragmatic Look at TDD in Ruby on Rails

How Red–Green–Refactor keeps SaaS codebases shippable as they scale — and why pragmatic TDD pays compounding dividends for Rails teams.

5 Min. ReadRead more →

The Algorithmic Trust Paradox: How iOS 26 and FinanceKit Are Rewiring Fintech After the AI Hallucination Crisis

How Apple Intelligence hallucinations exposed fragile market microstructure, and why iOS 26's Liquid Glass UI and FinanceKit API are fundamentally reshaping fintech data provenance, algorithmic trading, and the death of screen scraping.

6 Min. ReadRead more →